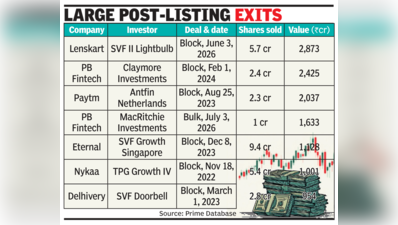

Bengaluru: Early investors in India’s listed startups have sold shares worth nearly Rs 97,252 crore since 2021, underscoring how public markets have emerged as the primary exit route for venture capital, private equity and other private-market investors after years of backing high-growth companies.Of this, PE and VC investors offloaded shares worth Rs 43,595 crore through the offer-for-sale (OFS) portions of 34 new-age technology IPOs, according to an analysis of Prime Database data. Identifiable exits through bulk and block deals after listing accounted for another Rs 53,657 crore. The analysis excludes promoter sales, broker transactions and routine secondary-market trades, while removing duplicate deal records.The exits span some of India’s biggest startup listings, including Paytm parent One 97 Communications, PB Fintech, Lenskart, Delhivery, Nykaa, Swiggy and Eternal (formerly Zomato). The latest came on July 3, when Temasek-backed MacRitchie Investments sold 1.02 crore shares in PB Fintech for Rs 1,633 crore. A month earlier, SoftBank’s SVF II Lightbulb sold Lenskart shares worth Rs 2,873 crore.The trend reflects a structural shift in India’s startup funding ecosystem. Unlike an earlier generation of companies that tapped public markets primarily to raise growth capital, startups today stay private for much longer, raising multiple rounds from angel investors, venture funds and private equity before listing. By the time they go public, an IPO is no longer just a fundraising exercise—it also marks the start of a staggered liquidity event for early investors.However, listing does not automatically signal the end of a venture investor’s ownership, said Ashish Agrawal, founding partner at Mettle Capital.“An IPO isn’t an exit event in itself. It simply marks the transition of a company from being privately held to publicly listed,” he said. While some investors prefer to monetise their holdings once liquidity becomes available, others continue to stay invested. Mettle evaluates a company’s operating performance, the incremental returns it can generate and the remaining life of its fund before deciding when to exit, Agrawal said.Pranav Haldea, managing director at Prime Database, said the role of IPOs has fundamentally changed over the past decade.“Between 1989 and 2012, shares sold by existing shareholders accounted for only 13.5% of the total IPO issue size, with the bulk comprising fresh capital raised by companies,” he said. “Today, private investors provide much of the growth capital before listing, making IPOs an important avenue for investor exits. It reflects the maturation of India’s capital markets.”That shift also reflects the economics of venture investing. Most VC and PE funds have finite lifecycles and are expected to return capital to their own investors within a defined timeframe.Rahul Chowdhri, partner at Stellaris Venture Partners and an early backer of Honasa Consumer, said exits should not automatically be interpreted as a vote of no confidence in a company. “VC funds are structured to exit over time. They are early-stage specialists, not long-term public-market fund managers,” he said. Funds often sell gradually rather than exiting completely at the IPO, particularly if they believe the listing valuation does not fully reflect the company’s long-term potential. By the time lock-in periods expire, many investors have also stepped off company boards and no longer possess the informational advantage they enjoyed as private shareholders.Anand Prasanna, managing partner at Iron Pillar, said venture funds typically operate for around a decade, making exits inevitable as they approach maturity—even from their strongest portfolio companies. “That often creates opportunities for large institutional public-market investors to build meaningful stakes in high-quality companies,” he said.A successful listing, however, does not guarantee sustained performance in the public markets.Sanjeev Yamsani, partner at Ventureast, said companies ultimately need what he calls the “trinity” of enduring value creation: differentiated technology, profitability with capital efficiency, and market leadership.“For early investors, the IPO increasingly marks the final stage of a long ownership journey,” he said. “For the company, it marks the beginning of life under a new set of shareholders who demand sustained execution and performance.”